Installment Sales

What is an installment sale and how do I report it?

In this talk, I’ll go through what an installment sale is and how it’s reported.

There are two characteristics that create an installment sale. First, is that payment for your property sold is received over 2 or more tax years. Second, there is a gain on sale or disposal of the property not a loss. Keep in mind there are specific rules for calculating a gain or loss on sale of property and for property used in a trade or business, recapture of depreciation may apply. Refer to my video on calculating gains and losses for more information.

You can use the install sale method rules, to report a portion of the gain on sale, each year, when you actually receive payment. The rules define calculating that gain each year based on the gross profit percentage, which is the percentage of the amount of profit divided by the total cost of the job. If you do not want to use the installment sale rules you can elect out of them by simply reporting the gain in full in the year of sale. To make this election you simply report the gain in full. The installment sale method rules are advantageous because they allow you to defer paying taxes on the sale until you have actually received the money.

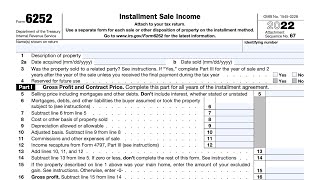

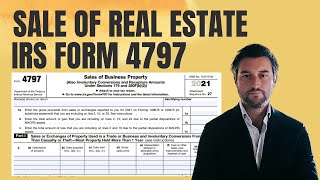

To report the gain in full during the year of sale, simply complete the relevant form to report the gain. For property used in a trade or business complete Form 4797 Sale of Business Property or for most personal use property, report the sale on Schedule D Capital Gains and Losses and Form 8949 Sales and Other Dispositions of Capital Assets. If you are using the installment sale method to calculate the portion of gain to recognize each year, then you complete Form 6252 Installment Sale Income, first, and then the relevant amount will flow to Form 4797 or schedule D and Form 8949, as required.

With an installment sale, there are few items to calculate.

First, the gain on the sale of the property in total. The gain is equal to the total proceeds received minus the adjusted basis in the property.

Second, is the amount of gain recognized during the current year, from the total year payments.

Third, is the interest income on the sale.

In brief, for calculating the gain on sale of property, everything of value you receive is considered the proceeds or sale price. This includes any property you receive, services provided or obligations like loans on the property that the buyer assumes on your behalf. Your adjusted basis in the property is subtracted from the total proceeds to equal the gain or loss. The adjusted basis begins with cost basis, which is usually what you paid for the property plus costs to get the asset ready for it’s intended use, which could be shipping and installation costs. However, there are specific rules for what can be included and excluded for different types of property.

So in summary, each installment sale payment you receive will usually be made up of 3 parts

Return of adjusted basis,

Gain on sale and

Interest income.

So why do we have to calculate these items for an installment sale? Well because the three items can all be taxed differently.

The adjusted basis in the property is a return on your investment and is not taxed, while interest income is always taxed at ordinary individual income tax rates and gains on sales may have special more favorable tax rates. All of the three amounts are calculated on the installment sale form 6252 and then flow to their relevant form to be reported. The installment sale form should be completed every year a payment is received.

Let’s talk a little more about the interest income. Because of the passage of time, an installment sale is effectively giving the buyer a loan. Therefore, an installment sale always has interest income. If an installment sale contract does not include interest income or it does not account for enough interest income then imputed interest must be calculated, which is called the unstated interest on the sale. This amount should then be ‘recharacterized,’ as interest income, instead of principal payment.

You may be wondering what is an adequate amount of interest? Well, the Applicable Federal Interest Rates, abbreviated AFRs, must be used. These rates are reported for each month and you should use the rate that was reported for the month of your sale. Note that even if you have a loss on a sale of property, if payments are received over multiple years then interest may still need to be imputed.

The installment sale rules do not apply in the following situations:

There is a loss on the sale of property

For sale of inventory

For sale of securities like stocks and bonds

![How to Calculate Taxable Gain from Selling a Rental [Tax Smart Daily 020]](https://i.ytimg.com/vi/VFqIr0GQKSk/mqdefault.jpg)

![Gifting Property to Your Children [Tax Smart Daily 014]](https://i.ytimg.com/vi/_MaWcMuimyo/mqdefault.jpg)

![How is reasonable compensation calculated? [Scorporation owner W2s]](https://i.ytimg.com/vi/RiwWU0WjuZk/mqdefault.jpg)