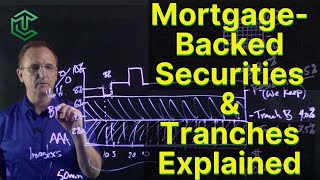

Lecture 2: Mortgage-Backed Securities (Pass-Throughs Agencies Prepayment Repos and Dollar Rolls)

This is the second installment of the Sunday evening lecture series, with a rigorous introduction to MBS. With passthrough notes short convexity and strips and derivatives fit for any investor profile, MBSs are a fascinating product. This video explains why prepayment risk leads to short convexity around small shifts in the parallel yield curve, how CPR (using PSA) and SMM measures are quoted, differences between TBA and Spec agency pools, differences between GSEs (Fannie and Freddie) and Ginnie, characteristics of private vs agency MBS and how repo funding using MBS paper differs from dollar rolling.

0:30: What is securitization and why securitize mortgages?

2:40: Why invest in MBS?

6:12: Flow of funds and tranching

9:46: Fixed income review, duration

13:00: Fixed income review, convexity

15:00: Why are MBS short convexity?

17:38: How does prepayment risk occur?

20:40: How do you measure prepayment? CPR, PSA, SMM and burnout

23:37: Graphical representation of payments P&I breakdown.

24:56: Effect of parallel shifts of interest rates: CPR, price, effective duration and effective convexity

28:01: Types of agency MBS: GSE (Freddie and Fannie) vs Ginnie

33:26: TBA vs Spec pools for Agency MBS

35:14: Buyers of agency MBS, pre/postcrisis

36:41: Privatelabel RMBS

41:59: Repo with MBS (repo books, overnight, term and open)

46:41: Dollar rolls: cheaper version of repos with MBS to avoid taking delivery, and returned securities do not have to be the same as the original security!

![Excel to Power BI [Full Course]](https://i.ytimg.com/vi/gjnnqsdvAc0/mqdefault.jpg)