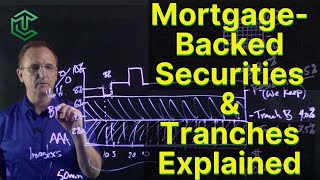

Mortgages and Mortgage-backed Securities (FRM Part 1 2023 – Book 3 – Chapter 18)

For FRM (Part I & Part II) video lessons, study notes, question banks, mock exams, and formula sheets covering all chapters of the FRM syllabus, click on the following link: https://analystprep.com/shop/unlimite...

AnalystPrep is a GARPApproved Exam Preparation Provider for FRM Exams

After completing this reading, you should be able to:

Describe the various types of residential mortgage products.

Calculate a fixedrate mortgage payment and its principal and interest components.

Describe the mortgage prepayment option and the factors that influence prepayments.

Summarize the securitization process of mortgagebacked securities (MBS), particularly the formation of mortgage pools, including specific pools and tobeannounceds (TBAs).

Calculate the weighted average coupon, weighted average maturity, single monthly mortality rate (SMM), and conditional prepayment rate (CPR) for a mortgage pool.

Describe the process of trading passthrough agency MBS.

Explain the mechanics of different types of agency MBS products, including collateralized mortgage obligations (CMOs), interestonly securities (IOs), and principalonly securities (POs).

Describe a dollar roll transaction and how to value a dollar roll.

Explain prepayment modeling and its four components: refinancing, turnover, defaults, and curtailments.

Describe the steps in valuing an MBS using Monte Carlo simulation.

Define Option Adjusted Spread (OAS) and explain its challenges and its uses.