Operating Section Statement of Cash Flows

In this video, we discuss the operating section for statement of cash flows.

Click to start your free trial: https://farhatlectures.com/

Operating Section of the Statement of Cash Flows

The operating section of the Statement of Cash Flows is crucial as it reveals how much cash has been generated or used by the company's core business operations over a specific period. This section provides insights into the cash effects of transactions that enter into the determination of net income, making it a vital tool for assessing the health and efficiency of a company’s primary activities.

1. Purpose of the Operating Section

The operating section helps stakeholders understand the cash inflows and outflows related to the company’s main business activities. It shows whether the company is able to generate sufficient cash from its core operations to sustain the business, pay dividends, repay debts, and fund future growth.

2. Components of the Operating Section

The operating section typically includes:

Cash Received from Customers: Represents the cash inflows from selling goods and services, which is the primary source of operational cash for most businesses.

Cash Paid to Suppliers and Employees: Represents the cash outflows for operating expenses, including payments for raw materials, services, and wages.

Interest Paid and Interest Received: Includes cash flows associated with interest expenses on debts and interest earned on cash holdings or shortterm investments.

Taxes Paid: Cash outflows related to various forms of taxation imposed on the company’s operations.

3. Calculation Methods

There are two main methods to prepare the operating section of the Statement of Cash Flows: the direct method and the indirect method.

Direct Method

Description: Lists major classes of gross cash receipts and gross cash payments. This method provides a clearer picture of where cash comes from and where it goes.

Example Entries:

Cash receipts from customers

Cash paid to suppliers

Cash paid to employees

Interest paid

Income taxes paid

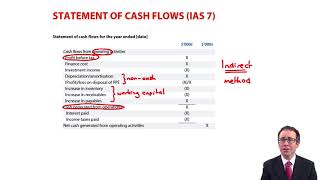

Indirect Method

Description: Starts with net income and adjusts for all noncash transactions, changes in working capital, and other items.

Steps:

Start with Net Income: From the income statement.

Adjust for NonCash Expenses: Add back depreciation, amortization, depletion, and any losses; subtract any gains associated with investing or financing cash flows.

Changes in Working Capital: Adjust for increases or decreases in current assets and current liabilities.

Example Adjustments:

Increase in Accounts Receivable: Subtract from net income.

Increase in Inventory: Subtract from net income.

Increase in Accounts Payable: Add to net income.

4. Advantages and Disadvantages

Direct Method:

Advantages: Provides a detailed view of cash flows.

Disadvantages: More challenging to prepare as it requires detailed information on cash transactions.

Indirect Method:

Advantages: Easier to prepare using information readily available from the accrualbased financial statements.

Disadvantages: Less transparent about the actual cash flows because it does not provide direct details of cash inflows and outflows.

5. Importance of the Operating Section

The operating section is particularly important for assessing:

Cash Generating Ability: The ability to generate cash from operating activities is a key indicator of a company’s viability.

Operational Efficiency: Effective cash management in operations reflects efficient control over cash inflows and outflows.

Sustainability: Consistent positive cash flow from operations often indicates a sustainable business model.

Conclusion

The operating section of the Statement of Cash Flows is a fundamental component that provides essential insights into a company's cash efficiency and operational effectiveness. Understanding this section is crucial for anyone looking to gauge the financial health and operational viability of a business.

#cpaexam #accountingmajor #accountingprinciples