Physical Observation of Inventory | Auditing and Attestation | CPA Exam

In this session , I will discuss physical observation of inventory.

✔Accounting students and CPA Exam candidates, check my website for additional resources: https://farhatlectures.com/

Connect with me on social media: https://linktr.ee/farhatlectures

#cpaexam #accountingstudent #auditcourse

Because inventory varies significantly for different companies, obtaining an understanding of the client’s industry and business is more important for both physical inventory observation and inventory pricing and compilation than for most audit areas. Examples of key considerations that auditors should consider include the inventory valuation method selected by management, the potential for inventory obsolescence, and the risk that consignment inventory might be intermingled with owned inventory. Auditors should evaluate whether risks related to inventory qualify as significant risks.

Auditors often first familiarize themselves with the client’s inventory by conducting a tour of the client’s inventory facilities, including receiving, storage, production, planning, and recordkeeping areas. The tour should be led by a supervisor who can answer questions about production, especially about any changes in internal controls and other processes since last year.

While gaining an understanding of the effect of the client’s business and industry on inventory, auditors assess client business risk to determine if those risks increase the likelihood of material misstatements in inventory.

Auditors have been required to perform physical observation tests of inventory since a major fraud involving the recording of nonexisting inventory was uncovered in 1938 at the McKesson & Robbins Company. The fraud was not discovered because the auditors did not physically observe the inventory, which at the time was not required.

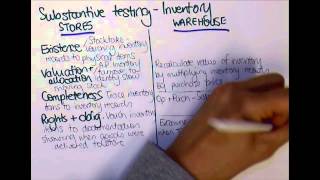

Auditing standards require auditors to satisfy themselves about the effectiveness of the client’s methods of counting inventory and the reliance they can place on the client’s representations about the quantities and physical condition of the inventories. To meet the requirement, auditors must:

Be present at the time the client counts its inventory for determining yearend balances

Observe the client’s counting procedures

Make inquiries of client personnel about their counting procedures

Make their own independent tests of the physical count

An essential point in the auditing standards is the distinction

An essential point in the auditing standards is the distinction between who observes the physical inventory count and who is responsible for taking the count. The client is responsible for setting up the procedures for taking an accurate physical inventory and actually making and recording the counts. The auditor is responsible for evaluating and observing the client’s procedures, including doing test counts of the inventory and drawing conclusions about the adequacy of the physical inventory.

Controls Over Physical Count

Regardless of the inventory recordkeeping method, the client must make a periodic physical count of inventory, but not necessarily every year. The physical count may be performed at or near the balance sheet date, at an interim date, or on a cycle basis throughout the year. The latter two approaches are appropriate only if there are adequate controls over the perpetual inventory master files.

Audit Decisions

The auditor’s decisions in the physical observation of inventory are similar to those made for other audit areas. They include selecting audit procedures, deciding the timing of the procedures, determining sample size, and selecting items for testing. The last three decisions are discussed next, followed by a discussion of the appropriate audit procedures.

Timing

The auditor decides whether the physical count can be taken before yearend primarily on the basis of the accuracy of the perpetual inventory master files. When a client does an interim physical count, which the auditor will agree to only when internal controls are effective, the auditor observes the inventory count at that time, and also tests transactions recorded in the perpetual inventory records from the date of the count to yearend. When the perpetual records are accurate and related controls operate effectively, it may be unnecessary for the client to count all the inventory at yearend.

Sample Size